A decade ago, investing in the stock market was something most middle-class Indian families avoided. It felt complicated, risky, and accessible only to those with insider knowledge or a broker uncle who knew how the system worked. Today, over 16 crore demat accounts are active in India — and the number grows by lakhs every month. College students are investing their pocket money in index funds. Salaried employees are building SIP portfolios alongside their PF contributions. Even homemakers are managing stock portfolios from their phones during afternoon hours.

The single thing that made all of this possible is the demat account. Without a demat account, you cannot buy a single share of any Indian company. You cannot invest in an IPO. You cannot hold mutual fund units in electronic form. You cannot participate in any of the wealth-building opportunities that India’s growing stock market offers. A demat account is not a luxury for serious investors — it is the basic infrastructure that every financially aware Indian needs in 2026.

The good news is that opening a demat account in India has never been easier. The entire process is now online, takes 15-20 minutes, requires minimal documentation, and can be completely free if you choose the right broker. This complete guide walks you through everything — what a demat account is, how it works, which broker to choose, the step-by-step opening process, charges to watch out for, and how to start investing once your account is active.

What is a Demat Account and Why Do You Need One

Demat stands for Dematerialised. A demat account is an electronic account that holds your financial securities — shares, bonds, ETFs, mutual fund units, government securities — in digital form. Just like a bank account holds your money digitally, a demat account holds your investments digitally.

Before demat accounts were introduced in India (1996), investors held physical share certificates — actual pieces of paper that represented ownership of a company. These certificates could be lost, forged, stolen, or damaged. Transferring shares required physical delivery of certificates, which took weeks and was expensive. The demat system eliminated all of these problems by converting everything to digital records maintained by two depositories — NSDL (National Securities Depository Limited) and CDSL (Central Depository Services Limited).

What a Demat Account Holds

- Equity shares of listed companies (BSE and NSE)

- Exchange Traded Funds (ETFs) — including index funds like Nifty 50 ETF

- Bonds and Non-Convertible Debentures (NCDs)

- Government Securities (G-Secs)

- IPO allotments

- Mutual fund units (if held in demat form)

- Sovereign Gold Bonds (SGBs)

- REITs (Real Estate Investment Trusts) and InvITs

The Demat Account Ecosystem

| Entity | Role |

|---|---|

| SEBI | Regulator — sets rules for all market participants |

| NSDL / CDSL | Depositories — maintain the actual demat records |

| Depository Participant (DP) | Your broker — the interface between you and the depository |

| Stock Exchange (NSE/BSE) | Where buying and selling of securities happens |

| Clearing Corporation | Settles trades — ensures money and shares change hands correctly |

When you open a demat account with Zerodha, Groww, Upstox, or any broker — you are actually opening a DP account with that broker. The broker is a Depository Participant registered with either NSDL or CDSL. Your actual securities are held by the depository, not the broker.

Types of Demat Accounts in India

Before opening an account, understand which type fits your situation.

Regular Demat Account

For Indian residents. This is what the vast majority of investors use. It allows you to hold all types of securities in electronic form and trade freely on Indian stock exchanges.

Basic Services Demat Account (BSDA)

Introduced by SEBI specifically for small investors. If the total value of securities in your demat account is below Rs. 2 lakh, you pay zero Annual Maintenance Charges (AMC). Between Rs. 2 lakh and Rs. 10 lakh, reduced AMC applies. Above Rs. 10 lakh, regular charges apply. This is ideal for beginners who are starting with small amounts.

Repatriable Demat Account (NRI)

For Non-Resident Indians (NRIs) who want to invest in Indian markets and repatriate (send abroad) their investment proceeds. Linked to an NRE (Non-Resident External) bank account.

Non-Repatriable Demat Account (NRI)

For NRIs who want to invest in India but do not need to repatriate proceeds. Linked to an NRO (Non-Resident Ordinary) bank account.

Demat Account vs Trading Account vs Bank Account

Many beginners confuse these three accounts. They are different and serve different purposes.

| Account | Purpose | What It Holds |

|---|---|---|

| Bank Account | Holds your money for transactions | Cash / Money |

| Demat Account | Holds your securities in electronic form | Shares, Bonds, ETFs |

| Trading Account | Platform to place buy/sell orders | Orders and Transaction History |

How they work together: When you buy shares, money moves from your bank account → through your trading account → to purchase shares → which are then stored in your demat account. When you sell shares, they leave your demat account → are sold through your trading account → and money comes back to your bank account.

Most modern brokers open all three accounts together (Demat + Trading + linked Bank Account) in a single application process, which is why most people refer to the entire setup simply as a “demat account.”

Choosing the Right Broker: Complete Comparison

This is the most important decision you will make. Your broker determines the platform you use, the charges you pay, the investment products available to you, and the quality of customer support you receive. In 2026, India has two broad categories of brokers.

Discount Brokers (Technology-First)

Discount brokers charge zero or very low brokerage for delivery trades (buying and holding shares) and a flat fee for intraday and F&O trades. They have excellent apps, fast execution, and low costs. They do not offer advisory services or relationship managers.

Full-Service Brokers (Traditional)

Full-service brokers charge higher brokerage (typically 0.3-0.5% per trade) but offer advisory services, research reports, dedicated relationship managers, and more comprehensive products including NPS, insurance, and global investing.

Top Brokers Comparison 2026

| Broker | Account Opening | AMC | Brokerage (Delivery) | Brokerage (Intraday) | Best For |

|---|---|---|---|---|---|

| Zerodha | Free | Rs. 300/year | Zero | Rs. 20 or 0.03% | Active traders, serious investors |

| Groww | Free | Free | Zero | Rs. 20 or 0.05% | Beginners, mutual funds |

| Upstox | Free | Free | Zero | Rs. 20 or 0.05% | Beginners, low-cost trading |

| Angel One | Free | Free | Zero | Rs. 20 or 0.25% | Beginners + advisory |

| Paytm Money | Free | Free | Zero | Rs. 10 or 0.05% | Beginners, mutual funds |

| ICICI Direct | Free | Rs. 700/year | 0.55% | 0.275% | Full-service, NRI accounts |

| HDFC Securities | Free | Rs. 750/year | 0.50% | 0.25% | Banking customers |

| Kotak Securities | Free | Rs. 600/year | 0.49% | 0.24% | Full-service |

| 5Paisa | Free | Rs. 400/year | Zero | Rs. 20 | Low-cost, active traders |

| Motilal Oswal | Free | Rs. 400/year | Zero | Rs. 20 | Research-backed investing |

Which Broker Should You Choose?

If you are a complete beginner: Groww or Upstox — simplest interface, zero charges, excellent for starting with mutual funds and then moving to stocks

If you want the best trading platform: Zerodha — India’s largest broker by active clients, excellent Kite platform, best charting tools, strong support

If you are a banking customer: ICICI Direct, HDFC Securities, or Kotak Securities — seamless integration with your existing bank account, though charges are higher

If you want advisory alongside investing: Angel One or Motilal Oswal — offer research reports and basic guidance along with execution

Our recommendation for most first-time investors in 2026: Start with Groww or Zerodha. Both are SEBI-registered, trusted by crores of investors, have excellent mobile apps, and charge zero for delivery (long-term) investing. You can always open a second account with another broker later.

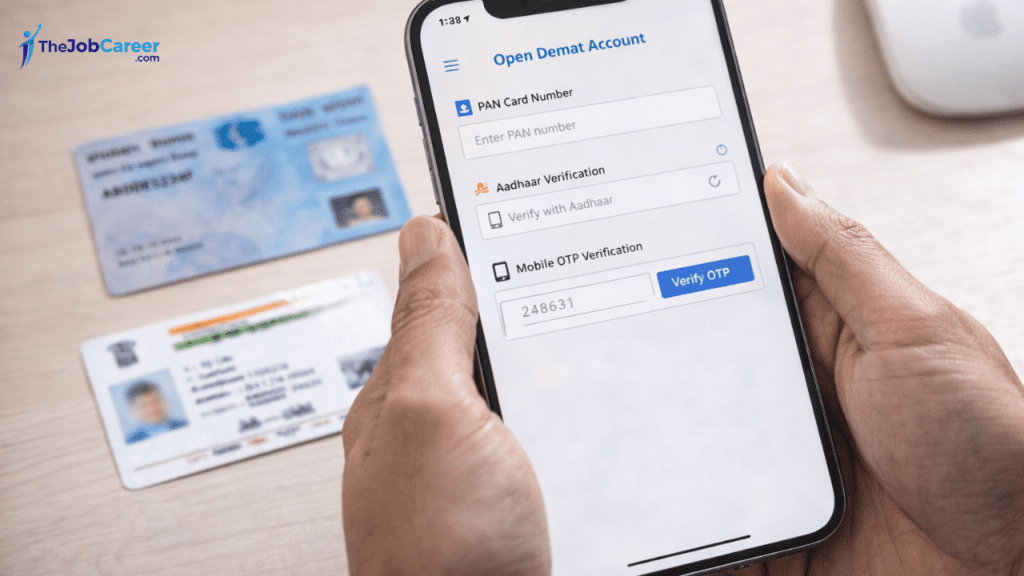

Documents Required to Open a Demat Account

The documentation process is now fully digital — you upload scanned copies or photos from your phone. No physical documents need to be sent anywhere.

Mandatory Documents

| Document | Purpose | Accepted Format |

|---|---|---|

| PAN Card | Mandatory — primary identity for all financial accounts | Clear photo or scan |

| Aadhaar Card | Address proof + Aadhaar-based e-KYC | Clear photo or scan |

| Bank Account Details | Linking bank account for fund transfers | Cancelled cheque OR bank statement |

| Signature | For account verification | Black ink on white paper, scanned |

| Photograph | Identity verification | Recent passport-size, white background |

For Income Proof (Required for F&O Trading)

If you want to trade in Futures and Options (F&O), most brokers require income proof:

- Last 6 months bank statement

- Latest ITR (Income Tax Return)

- Salary slip (last 3 months)

- Networth certificate from CA

For basic equity investing and mutual funds, income proof is not required.

For Minor Accounts (Under 18)

- Guardian’s PAN and Aadhaar

- Birth certificate of minor

- Relationship proof

Step-by-Step: How to Open a Demat Account Online

We will walk through the process using Zerodha as the example since it is India’s most popular broker. The process is similar across all major discount brokers.

Step 1: Visit the Broker’s Official Website or App

Go to zerodha.com (or download the Zerodha app). Always use the official website — never click links from WhatsApp or email claiming to be from any broker. Click “Open an Account” or “Sign Up.”

⚠️ Warning: Verify the website URL carefully. Fraudsters create fake broker websites with similar URLs. Zerodha’s only official URL is zerodha.com — not zerodha.net, zerodha.in, or any variation.

Step 2: Enter Your Mobile Number and Email

Enter your mobile number — this becomes your primary login identifier. Enter your email address. You will receive OTPs on both for verification. Verify both OTPs before proceeding.

Step 3: Enter Your PAN Card Details

Enter your PAN number. The system will automatically verify it against the Income Tax database. Your name as per PAN will be auto-populated — make sure it matches exactly with your other documents. If there is a mismatch, the account opening may be delayed.

Step 4: Complete Aadhaar-Based e-KYC

This is the fastest part of the process. You have two options:

Option A — DigiLocker Aadhaar (Recommended): Link your DigiLocker account to fetch your Aadhaar details automatically. This is instant and paperless. You do not need to upload any document.

Option B — Aadhaar OTP: Enter your 12-digit Aadhaar number. An OTP is sent to your Aadhaar-linked mobile number. Enter the OTP to verify your identity and address instantly.

Note: Your Aadhaar must be linked to your current mobile number for OTP-based verification. If it is not linked, you may need to use the manual document upload route.

Step 5: Upload Required Documents

If e-KYC is not fully completed through DigiLocker, you may need to upload:

- Clear photo of your PAN card (front)

- Clear photo of your Aadhaar card (front and back)

- Cancelled cheque OR 3-month bank statement showing your account number and IFSC

- Your photograph (taken in real time via phone camera or uploaded)

- Your signature on white paper (scanned or photographed clearly)

Photo Quality Tips:

- Take photos in good lighting — avoid shadows on documents

- Ensure all four corners of the document are visible

- Text should be clearly readable

- File size should be under 1-2 MB (compress if needed)

Step 6: Fill in Your Personal and Financial Details

You will be asked to fill in:

- Date of birth

- Father’s name (as per PAN)

- Marital status

- Annual income range (for risk profiling)

- Trading experience (first time, less than 1 year, 1-3 years, etc.)

- Politically Exposed Person (PEP) status — answer No if not applicable

- Bank account number and IFSC code

Step 7: Complete In-Person Verification (IPV)

SEBI regulations require In-Person Verification for demat account opening. In 2026, this is done through a 30-second live video selfie — you look at the camera, show your PAN card clearly, and sometimes read out a randomly generated code displayed on screen.

This process is done entirely through your phone’s camera within the broker’s app. It takes under 2 minutes and can be done anytime.

Step 8: E-Sign the Application

After all details are filled and documents uploaded, you need to digitally sign your application using Aadhaar-based e-Sign:

- Click “e-Sign with Aadhaar”

- Enter your Aadhaar number

- An OTP is sent to your Aadhaar-linked mobile

- Enter the OTP

- Your digital signature is applied to the application

This is legally equivalent to a physical signature and completes the application process.

Step 9: Pay the Account Opening Fee (If Applicable)

Most discount brokers — Zerodha, Groww, Upstox, Angel One — charge zero for account opening in 2026. Some charge a one-time fee of Rs. 200-500 for the demat account opening. Pay via UPI, net banking, or debit card if charged.

Step 10: Wait for Account Activation

After submission, your application goes through verification. Processing time:

| Broker | Typical Activation Time |

|---|---|

| Zerodha | 1-2 business days |

| Groww | Same day — 24 hours |

| Upstox | Same day — 24 hours |

| Angel One | 1-2 business days |

| ICICI Direct | 2-3 business days |

You will receive your Client ID (also called DP ID or UCC — Unique Client Code) and login credentials via email and SMS once the account is activated. This Client ID is your demat account number.

Charges You Must Know About

Understanding demat account charges prevents unpleasant surprises later. Here is a complete breakdown:

Account Opening Charges

Most discount brokers charge zero for account opening. Some full-service brokers charge Rs. 500-1,000 one-time.

Annual Maintenance Charges (AMC)

This is the yearly fee to maintain your demat account.

| Broker | Annual AMC |

|---|---|

| Zerodha | Rs. 300 |

| Groww | Free |

| Upstox | Free |

| Angel One | Free (first year), Rs. 240 thereafter |

| ICICI Direct | Rs. 700 |

| HDFC Securities | Rs. 750 |

BSDA Option: If your portfolio value stays below Rs. 2 lakh, you can opt for Basic Services Demat Account and pay zero AMC regardless of broker.

Brokerage Charges

| Trade Type | Discount Brokers | Full-Service Brokers |

|---|---|---|

| Delivery (Long-term holding) | Zero | 0.3% — 0.55% per trade |

| Intraday | Rs. 20 or 0.03% (whichever lower) | 0.1% — 0.275% |

| F&O (Futures & Options) | Rs. 20 per order | 0.1% — 0.3% |

Transaction Charges (Government Levies — Applicable to All)

These are fixed charges levied by SEBI, stock exchanges, and the government — applicable to every broker:

| Charge | Rate |

|---|---|

| Securities Transaction Tax (STT) — Delivery | 0.1% on sell side |

| Securities Transaction Tax (STT) — Intraday | 0.025% on sell side |

| Exchange Transaction Charges | 0.00297% — 0.00322% |

| SEBI Turnover Fees | Rs. 10 per crore |

| GST | 18% on brokerage + transaction charges |

| Stamp Duty | 0.015% on buy side (delivery) |

| DP Charges (on selling) | Rs. 13.5 + GST per scrip per day |

Note: DP charges (Depository Participant charges) of approximately Rs. 15-16 are charged every time you sell shares — this is separate from brokerage and is paid to the depository. Most beginners are surprised by this charge.

How to Add Money and Start Investing

Once your demat account is active:

Step 1: Add Funds to Your Trading Account

- Login to your broker’s app

- Go to “Funds” → “Add Funds”

- Enter the amount

- Pay via UPI (instant), Net Banking (instant), or NEFT/RTGS (takes time)

- Funds reflect immediately for UPI and net banking

Step 2: Search for a Stock or Mutual Fund

- Use the search bar to find the stock (e.g., “Reliance Industries” or “RELIANCE”)

- For mutual funds — search by fund name (e.g., “Nifty 50 Index Fund”)

- For ETFs — search by ETF name (e.g., “Nifty BeES”)

Step 3: Place a Buy Order

For stocks, you have two order types:

Market Order: Buys at the current market price immediately. Fast but you get whatever price is available.

Limit Order: You specify the maximum price you are willing to pay. Order executes only if the stock reaches that price. Recommended for beginners.

Step 4: Monitor Your Portfolio

After purchase, your shares will appear in your demat account after T+1 settlement (next trading day). You can monitor your portfolio value, returns, and individual stock performance through the broker’s app.

Demat Account Safety: Protecting Your Investments

With crores of rupees in demat accounts, safety is critical. Follow these practices:

Use strong, unique passwords: Never use your date of birth, phone number, or simple sequences as passwords. Use a combination of letters, numbers, and symbols.

Enable two-factor authentication (2FA): All major brokers support 2FA via OTP or TOTP (Time-based One-Time Password apps like Google Authenticator). Enable it immediately.

Never share your credentials: No broker, SEBI official, or any legitimate authority will ever call you asking for your trading password or OTP. If someone does, it is a fraud attempt — disconnect immediately.

Set up a DDPI (Demat Debit and Pledge Instruction): This is a one-time digital authorisation that allows your broker to debit shares from your demat account when you sell — replacing the old Power of Attorney (POA) system. Without DDPI, you need to manually authorise each sell transaction. Complete this setup when you open your account.

Monitor your demat holdings regularly: Check your Consolidated Account Statement (CAS) from CDSL or NSDL monthly to verify all holdings are accurate. Any discrepancy should be reported immediately.

Register for CDSL/NSDL SMS and email alerts: Both depositories send alerts for every transaction in your demat account. Register your mobile number and email to receive these alerts — they are your first line of defense against unauthorised activity.

Common Mistakes First-Time Demat Account Holders Make

Opening multiple accounts without understanding why: Many beginners open accounts with 3-4 brokers simultaneously. This leads to scattered investments, multiple AMC charges, and confusion. Start with one broker, learn the platform well, and only open a second account when you have a specific need.

Not checking AMC charges: Paying Rs. 700-750 per year in AMC to a full-service broker while holding only Rs. 50,000 worth of investments is a terrible deal. Always match your account type and broker to your portfolio size.

Trading intraday without adequate knowledge: Intraday trading (buying and selling within the same day) requires significant skill, discipline, and understanding of markets. Most beginners who start intraday trading lose money. Focus on long-term investing first — buy good stocks or index funds and hold them.

Investing based on tips from WhatsApp groups: WhatsApp “stock tips” groups are among the most common sources of investment fraud in India. Never invest based on unsolicited tips from unknown sources. Always research before investing.

Ignoring charges when calculating returns: A 1% annual return on a portfolio is meaningless if you are paying 0.5% in brokerage, 0.3% in AMC, and transaction charges on every trade. Understand your total cost of investing.

Not nominating anyone: Always add a nominee to your demat account. In the unfortunate event of the account holder’s death, the securities can be transferred to the nominee smoothly. Without a nominee, the legal heir must go through a complex and time-consuming process.

Frequently Asked Questions

Q1: Can I open a demat account without a PAN card?

No. PAN card is mandatory for opening a demat account in India. SEBI regulations require PAN for all financial market transactions. If you do not have a PAN card, apply for one first — it typically takes 7-15 working days. You can apply online at onlineservices.nsdl.com or utiitsl.com.

Q2: Can a minor open a demat account?

Yes. Minors can hold demat accounts, but the account is operated by a guardian (parent or legal guardian) until the minor turns 18. Upon turning 18, the account must be converted to a regular account by providing fresh KYC documents.

Q3: How many demat accounts can I have?

You can hold multiple demat accounts with different brokers — there is no legal restriction. However, each account attracts its own AMC and maintenance requirements. Most investors find one or two accounts sufficient.

Q4: Is my money safe if my broker shuts down?

Yes. Your shares are held by the depository (NSDL or CDSL) — not by the broker. If a broker shuts down, your shares remain safe in the depository. You can transfer them to another broker. However, cash lying in your trading account (not yet invested) could be at risk — always transfer uninvested funds back to your bank account.

Q5: What is the difference between NSDL and CDSL?

Both NSDL and CDSL are depositories — they maintain electronic records of securities. NSDL was established first (1996) and is associated with NSE. CDSL was established in 1999 and is associated with BSE. Both are equally safe, regulated by SEBI, and backed by major financial institutions. Your broker’s choice determines which depository your account is with.

Q6: How long does it take to open a demat account completely online?

The application process itself takes 15-20 minutes if all your documents are ready. Account activation after submission takes 1-48 hours depending on the broker. With brokers like Groww and Upstox, many accounts are activated the same day.

Q7: Can I open a demat account if I am a student with no income?

Yes. There is no minimum income requirement to open a demat account. Students can open accounts and start investing even with very small amounts. Many stocks and ETFs can be bought for under Rs. 100. However, if you want to trade in F&O (Futures and Options), income proof is required — basic equity investing has no such requirement.

Q8: What happens to my demat account if I do not use it?

If your demat account has zero transactions for a year, it may become “dormant.” A dormant account can be reactivated by submitting a reactivation request along with fresh KYC documents to the broker. Your securities remain safe during this period — they do not disappear. However, AMC charges continue to accrue.

Conclusion: Your Demat Account Action Plan

Opening a demat account is one of the most straightforward and impactful financial steps you can take in 2026. It takes 20 minutes, costs nothing with the right broker, and opens access to the wealth-building power of India’s growing stock market — which has delivered an average annual return of 12-15% over the long term.

Here is exactly what to do this week:

- Choose your broker — for most beginners, Groww or Zerodha are the strongest starting points

- Keep your PAN card, Aadhaar, cancelled cheque, and a blank white sheet for your signature ready

- Ensure your mobile number is linked to your Aadhaar (verify at myaadhaar.uidai.gov.in)

- Visit the official broker website — never a third-party link

- Complete the application in one sitting — it takes 20 minutes

- Once activated, start with a small amount — Rs. 1,000 in a Nifty 50 index fund is a perfectly valid first investment

- Add a nominee and enable 2FA before doing anything else

The earlier you open a demat account and start investing — even small amounts — the more time your money has to grow. The eighth wonder of the world is compounding — and it works only if you start.

Start today. Invest wisely. Build wealth steadily.

All the best! 💰

Related Learn & Growth Articles:

- Global Investing: A Complete Guide for Indian Investors in 2026

- What Are Sovereign Gold Bonds? Meaning, Interest Rate, Tax Benefit and How to Invest

- How to Apply for PAN Card Online in India: Step-by-Step Guide

- 7 Common Job Frauds in India: Complete Awareness Guide

- Digital Arrests: Inside India’s Scariest Scam and How to Stop It

- LinkedIn Profile Guide 2026: How to Get Noticed by Recruiters

Related Career Articles:

- Top 10 High Paying Jobs in India 2026

- Freelancing in India 2026: How to Start, Earn and Grow Your Income

- Fresher Jobs Rs. 20,000 Salary — No Experience Required

- Work From Home Jobs 2025: Best Online Opportunities

- How to Switch Careers at 30-35-40: Complete Roadmap

Official Resources:

- SEBI Official: https://www.sebi.gov.in

- NSDL: https://www.nsdl.co.in

- CDSL: https://www.cdslindia.com

- NSDL CAS (Holdings Statement): https://www.cams.co.in

- Aadhaar Linking Status: https://myaadhaar.uidai.gov.in

- PAN Card Application: https://www.onlineservices.nsdl.com

Broker Official Websites:

- Zerodha: https://zerodha.com

- Groww: https://groww.in

- Upstox: https://upstox.com

- Angel One: https://www.angelone.in

- Paytm Money: https://www.paytmmoney.com